CIT and limited partnerships

The inclusion of limited partnerships in CIT will increase the burden on tens of thousands of Polish entrepreneurs

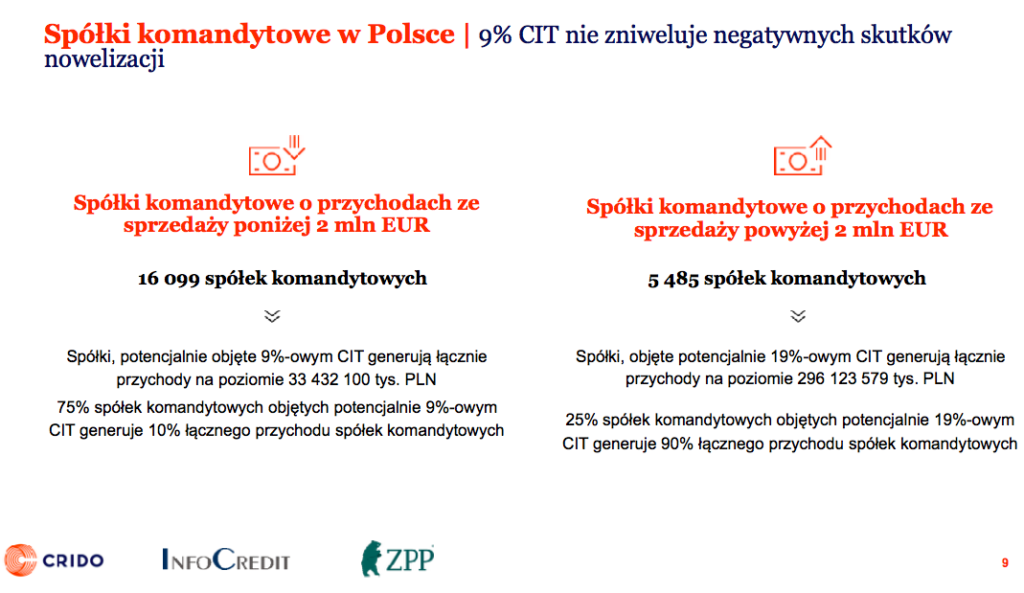

The inclusion of limited partnerships in the CIT tax will lead to a significant increase in taxes for nearly 73,000 Polish entrepreneurs.

The most dynamic businesses will suffer the most, as they will not have the chance to benefit from the lower 9% CIT rate, and the actual taxation of partners in these partnerships will increase to 34%-38% instead of the current 19%-23%.

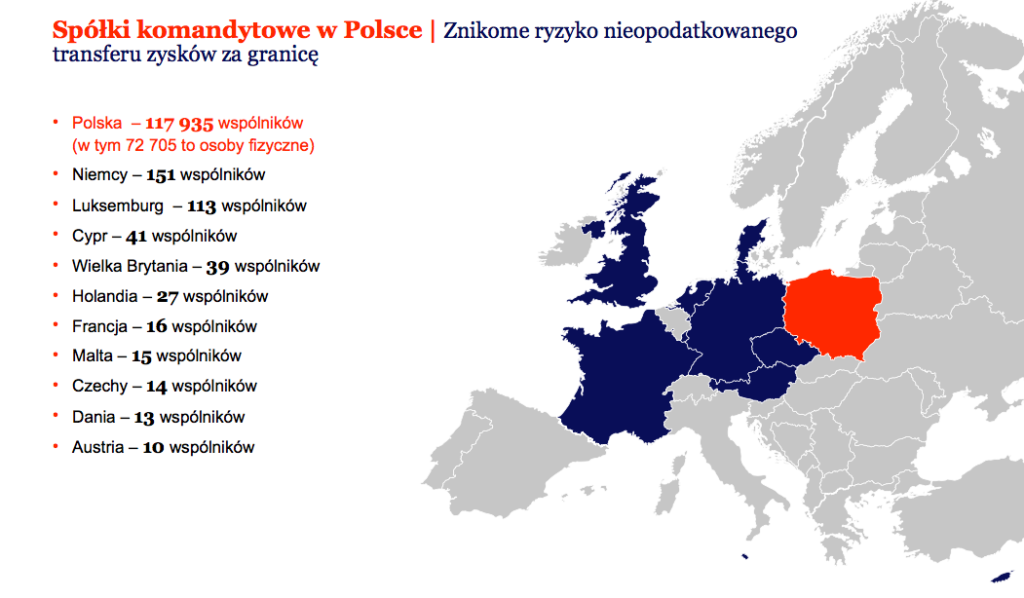

Only 1% of limited partnerships have foreign partners, and their share in the total number of partners in limited partnerships is 0.4%, which means that the potential risk of untaxed transfer of profits abroad is marginal

– according to a report presented during a joint conference of CRIDO, ZPP and InfoCredit.

Consequences for business

In connection with the planned tax changes (as of October 2, 2020), there will be a significant increase in the tax rate for nearly 73,000 Polish entrepreneurs. Around 75% of companies with lower turnover will be able to benefit from a 9% CIT rate instead of 19%. However, as many as 25% of limited partnerships responsible for 90% of the revenues generated by these businesses (i.e. nearly PLN 300 billion per year!) will pay 19% CIT. Effectively, the interest rate for partners in these companies, mainly Polish entrepreneurs, will increase to 34% or, in the case of people paying the solidarity levy, to 38%.

Even Estonian CIT will not help

The new tax benefit in the form of the so-called Estonian CIT does not cover limited partnerships. Even assuming that some entrepreneurs decide to transform into a capital company (LLC or S.A.), it will probably also remain, apart from this, a preferential tax regime – this form of activity is popular in particular among entrepreneurs operating in the trade and services industry, which means no investment expenses that are a condition for using this form of taxation.

Limited partnerships are not commonly used for international tax optimization

Contrary to the justification of the planned changes, the data do not indicate that limited partnerships are used in international tax optimization schemes. In Poland, approximately 43,000 limited partnerships conduct active business activity. According to the analysis of CRIDO experts, based on data from the InfoCredit database, 92% of limited partnerships are businesses run by individuals from Poland. 72,705 thousand Poles run their businesses in this form.

For comparison, only 0.4% of partners in limited partnerships in Poland come from abroad. In first place are Germany (151 partners), for whom this form of running a business is quite common and which is indicated as one of the reasons for Germany’s economic success. In subsequent places are Luxembourg (113 partners), Cyprus (41) and Great Britain (39).

We are talking about the entire country and many industries

Limited partnerships are scattered all over the country. The largest number of them are in the following voivodeships: Mazowieckie (11,290), Wielkopolskie (5,611), Małopolskie (4,744) and Śląskie (3,792). They operate in various industries, most of them deal with industrial processing, construction and trade. Many transport and logistics companies and the catering industry also operate in this way. This form has allowed more than one Polish entrepreneur to develop, who, having a “flair” for business and running it, was able to simultaneously limit the risk for his family.

– The combination of single taxation at the rate of 19% with limiting the risk of running a family business is a positive incentive and motivator for the development of entrepreneurship. This is shown by the example of Germany, whose economic power grew precisely on family businesses run in the form of limited partnerships. The planned double taxation of limited partnerships will not only be a negative signal for Polish, committed entrepreneurs, but will also put domestic companies in a worse market position in relation to their foreign competitors. Taking into account the EU directive, the so-called Parent-Subsidiary, a foreign investor from the EU will pay no more than 19% of income tax – comments Mateusz Stańczyk, partner at CRIDO.

– Including limited partnerships in the CIT tax is a bad idea. The data does not indicate that these are entities used for international optimization schemes. However, they are an attractive form of conducting business for Polish, dynamically developing businesses. It should be emphasized that this is another proposal to increase the burden of taxes, which has appeared in a relatively short time. Meanwhile, according to our research, the willingness of entrepreneurs to invest is the lowest in years – this is not happening without a reason. Multiple changes in regulations, the sudden introduction of new burdens, the lack of basic legal security for companies are the main reasons why the investment rate in Poland is far from the level of 25% of GDP expected according to the Strategy for Responsible Development – claims Jakub Bińkowski, director of the Department of Law and Legislation of the Association of Entrepreneurs and Employers.

– Today, more than ever before, every proposed change to the tax system should also be analyzed in the context of employment. Greater burdens for tens of thousands of Polish entrepreneurs may mean a reduced willingness to create new jobs or maintain existing ones. InfoCredit will soon conduct a survey among entrepreneurs so that they can assess the proposed changes to taxation in the context of employment and their market opportunities. We will share the results of this survey with you in October. The InfoCredit index has been signaling for many months that when there are fewer jobs, the number of sole proprietorships increases. And these have a much lower ability to achieve market success than companies with an established position – says Jerzy Wonka, InfoCredit Development Director.